- Fixed-rates mortgages: The pace remains the same into totality of your loan, and make monthly obligations foreseeable. Its popular getting repaired-price mortgages getting regards to either fifteen otherwise 3 decades.

- Adjustable-price mortgage loans (ARMs): The rate can change at specified minutes, which means that monthly premiums can move up otherwise down. Extremely Hands begin with a fixed speed to have ranging from step 3 and you can ten years.

Mortgage loans that aren’t considered conventional become FHA financing, that are covered because of the Government Property Government (FHA) or Va money, covered from the Agency from Veterans Issues (VA). FHA and you will Va fund succeed more comfortable for qualifying home buyers to track down accepted having home financing by removing the latest economic conditions and, most helpfully, the necessary advance payment number.

Conforming mortgage loans was an excellent subset regarding traditional mortgage loans you to meet up with the particular resource standards lay by the Fannie mae and Freddie Mac computer. (Fannie mae and you will Freddie Mac are bodies-sponsored people (GSEs) you to definitely buy mortgage loans out of loan providers and sell these to buyers.) Perhaps one of the most essential requirements is the amount borrowed. Getting 2023, brand new standard compliant loan restriction to possess a single-family home in the most common of the United states was $726,200, having high restrictions for the elements which have costly housing markets. Conforming money might also want to see almost every other direction about the newest borrower’s credit rating, debt-to-income ratio, therefore the loan-to-really worth proportion.

Non-compliant mortgages do not see criteria put because of the Government Casing Loans Institution (FHFA), Freddie Mac, and/otherwise Fannie mae. Jumbo funds is actually a form of low-compliant loan always pick properties higher priced as compared to compliant mortgage maximum. Jumbo loans possess highest rates and qualification criteria than simply conforming mortgages.

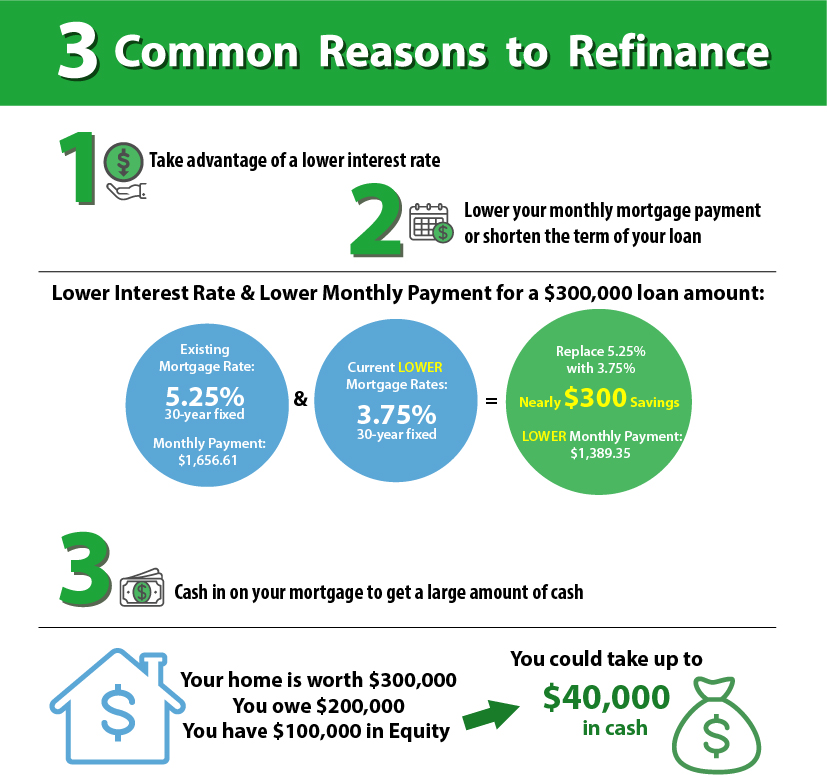

Knowledge home loan costs

Their home loan speed makes a big change in the way much you can easily shell out to purchase your house. Eg, between 2020 and you can 2023 the typical mortgage rate flower throughout 4% so you can nearly 8%. Getting a good $two hundred,000 31-season mortgage – before taxes and you may insurance coverage – might shell out:

- $1,468 a month from the 8%

- $955 30 days during the 4%

That’s an amazing $513 a month difference. Along the life of the 29-12 months mortgage you’d find yourself spending an extra $184,680 inside notice on 8% compared to the within cuatro%. Put simply, in the an effective 4% Annual percentage rate the brand new payment per month on the an effective $308,000 mortgage would be the equivalent of this new monthly payment into good $two hundred,000 financial on 8% Apr.

You should use our financial calculator observe significantly more examples of just how interest levels alter exactly how much you pay bad credit personal loans Nevada and exactly how far family you really can afford.

It’s vital to check around and examine costs off several lenders for the best bargain. Find out more about how your credit rating has an effect on financial prices.

Pre-approval against pre-degree

- Pre-qualification try a quick comparison of your capacity to pay for an effective financial, constantly according to care about-said economic pointers.

- Pre-recognition is far more on it and needs papers of your own credit history and you can credit history. It gives you a much better concept of the mortgage matter you might qualify for. A pre-approval is oftentimes expected prior to going around price to satisfy owner that you will be in a position to get investment.

Advance payment

When you find yourself 20% is oftentimes cited given that practical down payment to own old-fashioned mortgages, of numerous lenders give finance that need as little as step three% off getting first-big date homebuyers.

Saving good 20% advance payment isn’t any effortless activity. At the conclusion of 2023, the average household speed in america is $417,700. Who require a good 20% down-payment out of $83,540. A lowered downpayment causes it to be you can to shop for a good family much sooner, but boasts extra costs. Your own interest rate may be large and need to spend personal financial insurance policies (PMI) before mortgage-to-value ratio try lower than 80%.