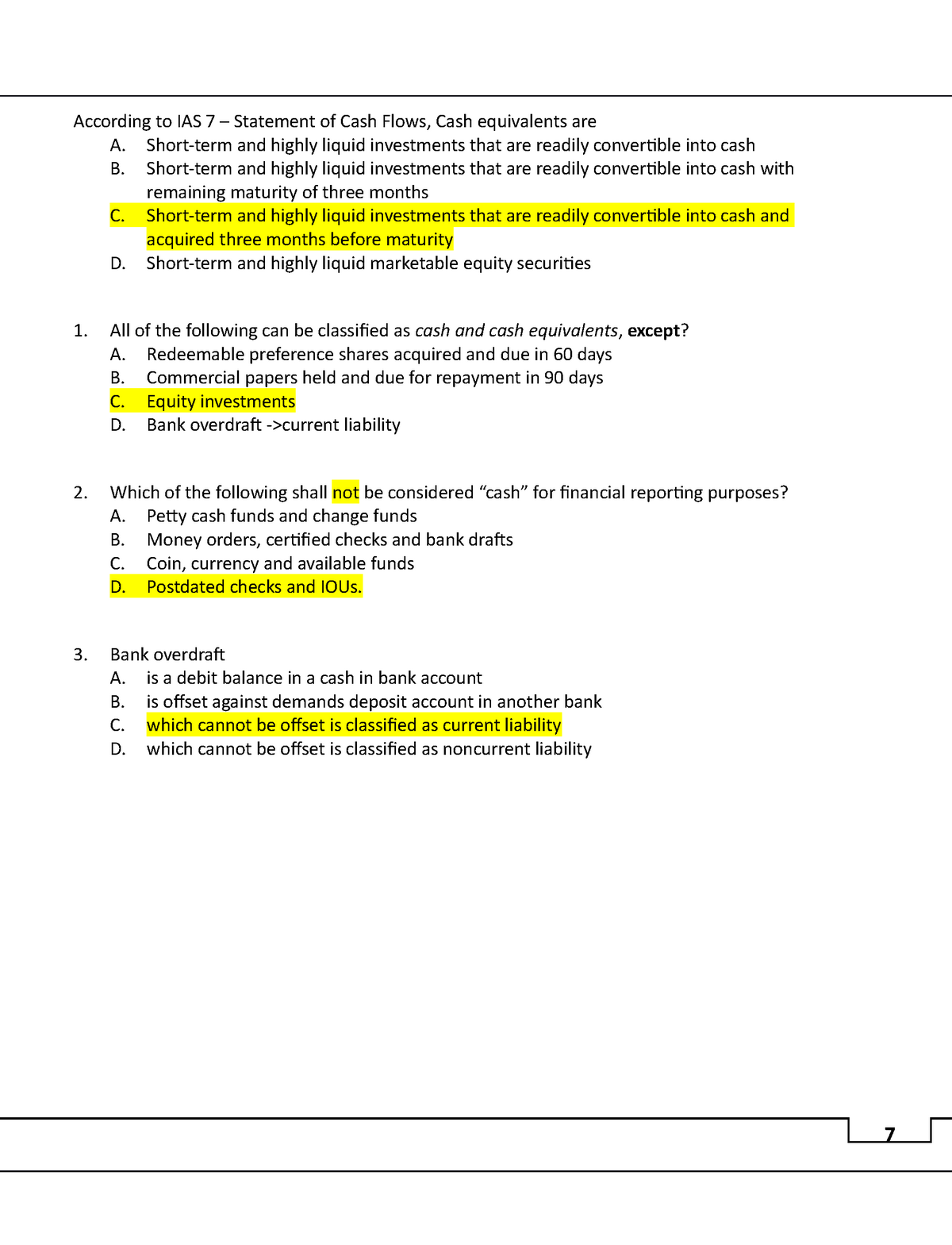

As previously mentioned above, discover FHA advice apps certain to Fl that assist borrowers secure funding. Below you will have informative data on probably one of the most popular down payment and closure costs recommendations applications in the condition. Every one of these mortgage apps is designed towards borrowers’ finest motives in mind.

Depending on the You.S. Service regarding Houses and Metropolitan Development’s website (hud.gov), you will find eight Statewide and you may Local FHA programs which will help you safer capital getting a house. Getting the full list and you can info on for every single, head to

Important: Keep in mind, any household becoming ordered with a loan-to-worthy of proportion above 80% (deposit less than 20%) will need home loan insurance coverage that is ount would-be similar to the homeowners’ plan, however, that it financial insurance is exactly what facilitate finance while making FHA financial apps you’ll be able to.

To buy a home using an enthusiastic FHA-acknowledged lender is a fantastic selection for basic-big date homeowners otherwise whoever might need down payment or closing cost guidelines. If you have any queries otherwise are curious about starting, reach out to Neighborhood Loans today!

Faq’s on FHA

Here are not a large number of variations or downsides so you’re able to choosing an enthusiastic FHA Loan. As the FHA apps keeps low down fee requirements you may not possess as much collateral of your home at the start of the loan. This will carry out a somewhat highest payment due to good highest dominating fee and dependence on PMI (listed above).

Just what disqualifies me personally regarding an enthusiastic FHA Loan?

The only reasoning you would rating declined getting an enthusiastic FHA home loan financing is if you are not able to generate a monthly home loan payment promptly. Lenders look at your credit rating and you can personal debt so you can money ratio to track down a beneficial end up being of your own financial history. Considering one to pointers, they will accept otherwise reject your having a home loan even although you rating refused, there are ways to replace your financials and return stronger. Certain loan providers will also make it easier loan places Greeley to lay out a decide to produce on course to purchase a property.

Perform Manufacturers Hate FHA Customers?

The fresh vendors of the home won’t hate you since somebody however FHA applications keeps even more inspections and requirements to track down from the finishing line. If discover so many requests from the vendor, a purchaser will be prone to refuse your own provide. Vendors should not set extra cash towards a home it was leaving and need the method going just like the smoothly as you’ll be able to. Whether they have numerous offers and want to sell punctual, they may just go with an informed and you will quickest promote.

Can FHA Fund end up being Refinanced?

Naturally! Any mortgage is refinanced if it meets the brand new qualification standards for the program. Furthermore doing their bank to make certain that refinancing tends to make monetary experience for you. Many reasons exist in order to re-finance incase you want to find out about all of them, look at the recommendations i’ve readily available.

Create FHA Loans Take more time to shut?

Nope! A great re-finance usually can end up being finished less than simply a buy once the they just involves providing your with the the latest financial words. Loan providers get various other turn-moments depending on how active they aremunicate together with your financing administrator to get a far greater estimate from the length of time the new refinance techniques usually takes to you personally.

How do i Remove Individual Financial Insurance coverage for the an enthusiastic FHA loan?

Private Mortgage Insurance rates (PMI) will become necessary if your loan-to-value (LTV) ratio is actually above 80%. Which have an FHA financing, you make a downpayment out-of roughly 5-10%, causing you to be which have an LTV of 95-90%. Since you build your monthly payments, you will see this new fee drop. Once you arrived at 80%, you could potentially request it to be got rid of, otherwise re-finance on the the newest words while also that have it taken out of your own monthly payment.